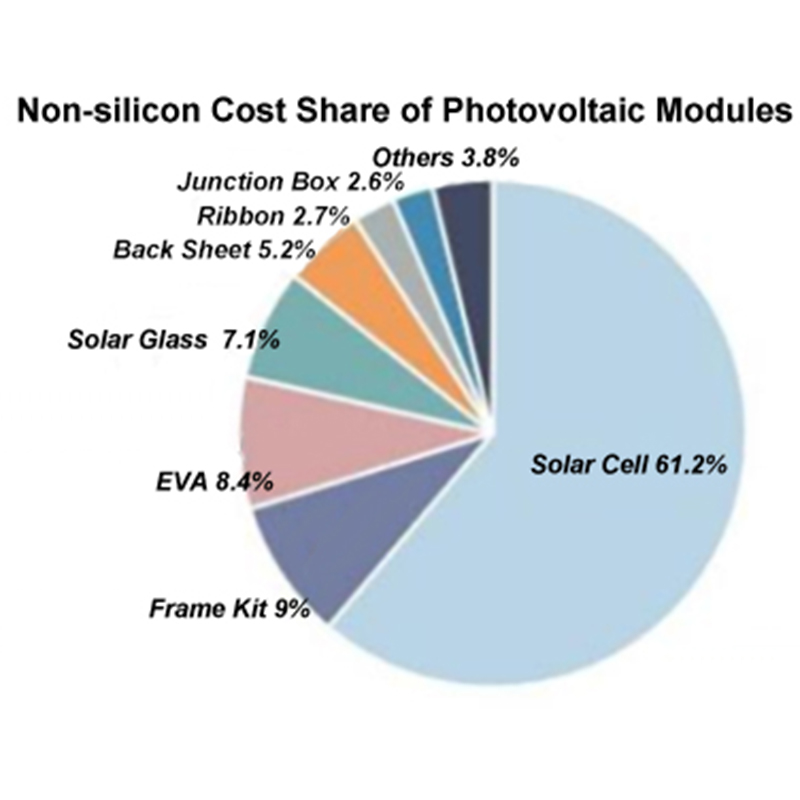

The role of photovoltaic glass is to protect the cell and extend its life and improve the efficiency of power generation. Cells account for 60% of the module cost, ranking first. It is closely followed by photovoltaic glass, which accounts for about 12 percent.

As with polysilicon and silicon wafers, China’s photovoltaic glass dominates the world, with a global market share of more than 90%.

1. Three major barriers create a duopoly

1) Resource Barriers

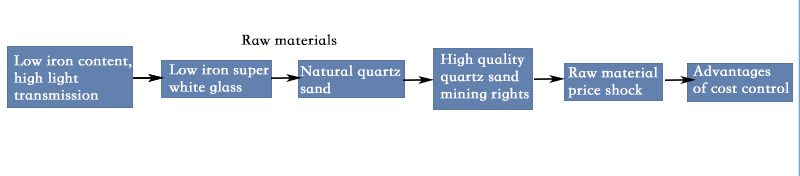

The raw materials of photovoltaic glass are quartz sand and soda ash, of which quartz sand is more scarce.

First of all, the iron content affects the light transmittance of glass. The higher the iron content, the lower the light transmission. High iron content will make the glass color lime green. The photovoltaic glass requirements for light transmission are very high, so the use of low-iron ultra-white glass.

Super white glass is made of natural quartz sand with very low iron content. However, this quartz sand is relatively scarce. Therefore companies with high-quality quartz sand mining rights can withstand the impact of raw material price fluctuations.

There are fewer quartz sand mining areas in China that are easy to mine, mainly in the south. With the capacity expansion of downstream components, scarce natural quartz sand resources will become more scarce. Therefore, companies that have already mastered high-quality ore sources have the advantage of cost control.

2) Technical Barrier

Photovoltaic glass has high light transmission requirements, and the corresponding technical content and energy consumption level are high. It is difficult for general glass manufacturers to switch to PV glass production by improving existing production lines, so the technical barriers are high.

3) Asset Barrier

As we all know, glass is a typical asset-heavy industry with a significant scale effect. Photovoltaic glass is no exception. The kiln is the most core and most invested equipment of the glass factory. Compared with small kilns, large kilns have low production costs and high yield rates, with costs 15% lower than small kilns and yield rates 10%-15% higher than small kilns. The large scale of investment means that the payback period is also long. Therefore, it is difficult for small enterprises to afford the financial strength. And large enterprises can reduce the production cost and thus open the gap.

2. Roller-coaster prices

From the gross margin level, the first echelon’s annual average gross profit in the past five years is 34.5%. The second echelon is 18.5%. The first echelon as a whole is 16% higher than the second echelon. This also confirms the significant cost control advantage of the leading companies.

In the second half of 2020, PV glass was restricted by capacity replacement. The average market price of 3.2mm specifications once soared to 43 yuan / ㎡. 2.0mm specifications of the average market price also rose to 35 yuan / ㎡. And this price level has continued until mid-March this year. It is so, 2021 quarterly report photovoltaic glass manufacturers to achieve high growth in revenue and net profit, net profit growth rate of more than twice the year-on-year.

3. The quantity and price will rise?

1) Double-sided components drive demand

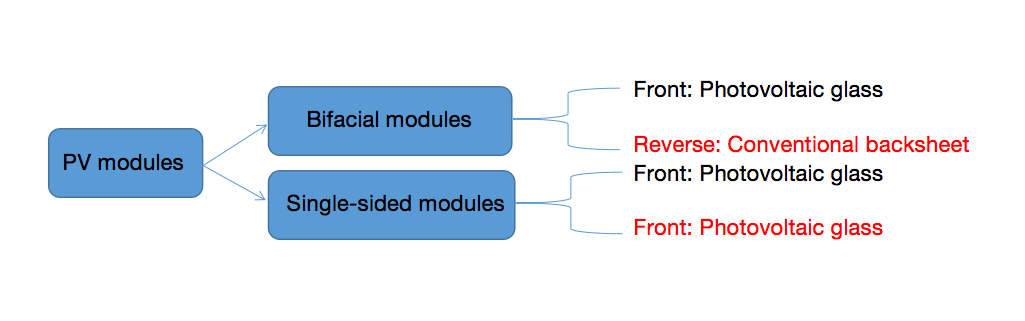

As we said before, cost reduction and efficiency has been the first driver of the PV industry, and bifacial modules are in line with this trend.

Compared with single-sided modules, bifacial modules have four main advantages.

First, both the front and back sides can absorb sunlight, thus increasing the module’s power generation by 10% to 30%;

Second, the photovoltaic glass is more durable than the traditional back sheet, which facilitates the extension of module life;

Third, the material is convenient for later recycling;

Fourth, the bezel accounts for 10% of the module cost, while bifacial modules do not need a bezel, thus avoiding the cost pressure caused by metal price fluctuations.

Therefore, bifacial modules will be the main development direction in the future.

2) The peak season of installation is coming

Generally, the fourth quarter is the peak season of installation, distributing photovoltaics whole county to promote. “Energy consumption double control” under the new energy represented by photovoltaics will gradually become mainstream. Combined with the glass price relaxation, downstream demand is expected to improve significantly. Photovoltaic glass prices are likely to rebound.

In the future, the improvement in demand overlapped with the release of capacity restrictions is expected to further promote the volume and price of photovoltaic glass…